Federal Reserve Holds Rates Steady Amid Inflation and Geopolitical Risk

Published: March 18, 2026

Updated: Today with the Federal Reserve’s decision

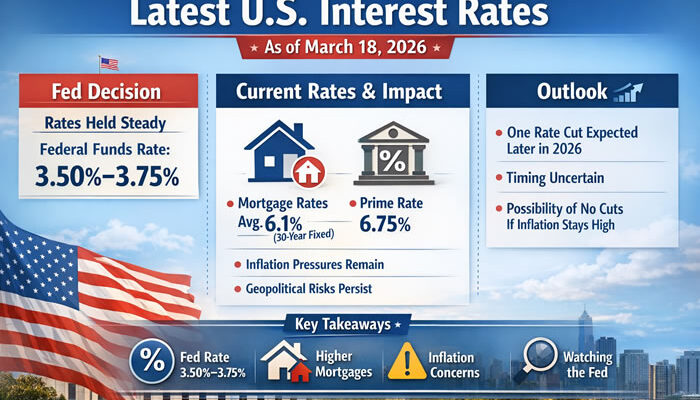

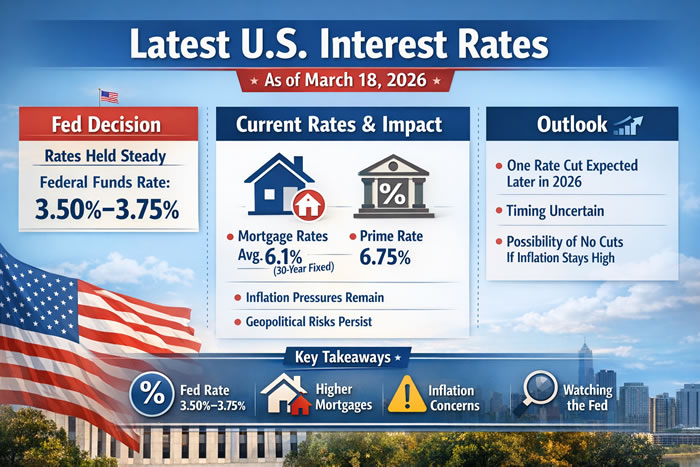

The U.S. Federal Reserve has kept its key interest rate unchanged, maintaining the **federal funds rate in the range of 3.50% to 3.75% at its March 18, 2026 meeting. This marks the second consecutive policy meeting in 2026 where rates have been held steady amid economic and geopolitical uncertainty.

What Happened With U.S. Interest Rates Today?

The Federal Open Market Committee (FOMC), chaired by Jerome Powell, announced that:

-

The **benchmark federal funds rate remains at 3.50%–3.75%.

-

This decision was widely expected by markets and reflects ongoing concerns about inflation and slowing economic momentum.

-

The Fed’s policymakers reiterated that they still expect just one rate cut in 2026, unchanged from last forecasts — even as geopolitical risks complicate the outlook.

The decision comes as inflation pressures persist, partly due to rising energy prices linked to geopolitical tensions in the Middle East, including the conflict with Iran.

Why the Fed Is Pausing on Rate Cuts

Although inflation remains above the central bank’s 2% target, the Fed is taking a cautious approach to changing rates. Factors influencing this stance include:

-

Higher commodity prices due to the Iran war, pushing inflation expectations up.

-

A cooling labor market, which could weigh on economic growth.

-

Uncertainty over the future inflation path, making policymakers hesitant to adjust monetary policy too rapidly.

Despite these concerns, most Fed officials still project only one rate cut later in 2026, though timing remains uncertain.

Current Impact on Consumers and Markets

While the federal funds rate itself influences short‑term lending between banks, several markets feel the effects:

-

Mortgage rates — The average U.S. 30‑year fixed mortgage rate recently climbed back above 6%, reflecting broader market conditions.

-

Prime lending rates — According to market reports, the U.S. prime rate remains around 6.75%, which influences borrowing costs for many consumers and businesses.

These higher borrowing costs make home loans, business credit, and consumer loans more expensive compared with previous years, limiting spending and investment.

Outlook: What’s Next for Interest Rates?

Economists and markets are currently weighing several scenarios for the rest of 2026:

-

One modest rate cut remains on the Fed’s projections, but timing could shift later in the year depending on inflation and labor data.

-

Some market forecasts now price in a delayed cut or even no cuts at all if inflation proves more persistent than expected.

-

Long‑term forecasts for mortgage and bond yields will continue to react to Fed guidance and macroeconomic sentiment throughout 2026.

In addition, banks and financial institutions continue to adjust their forecasts for rate movements based on evolving data and global developments.

What This Means for Borrowers and Investors

-

Borrowers should expect borrowing costs to remain elevated unless inflation data weakens significantly.

-

Investors are closely watching inflation reports, economic growth indicators, and geopolitical developments for clues on future Fed decisions.

-

Homebuyers may find mortgage rates remain influenced more by bond markets than direct Fed rate moves in the short term.

Summary: Key Takeaways

| Topic | Current Status |

|---|---|

| Federal Funds Rate | 3.50%–3.75% (unchanged) |

| Rate Cut Expectation (2026) | One cut projected by Fed officials |

| Impacting Factors | Inflation pressures, geopolitical risks, cooling labor market |

| Mortgage Rates | Around 6.1% average for 30‑year loans |